Playing Different Games

Or why Tiger is eating your lunch (& your deals)

The Tiger Phenomenon

Somewhere, right now, in Silicon Valley…

“So how about these Tiger guys eh?”

“Hah! You’re telling me — I heard they did [Deal X] in 24 hours after only getting a P&L for diligence and came in 25% over the founder’s asking price!”

“I heard they’re doing a new deal every 2 days! It’s completely crazy”

“Totally — good thing we’re sticking to our knitting, these hedge funds are insane”1

If you actively invest in private, high-growth technology businesses, there’s a good chance you’ve had a conversation that looks something like the above in the last 12 months. Or if you haven’t, you’ve almost certainly seen an investor on VC Twitter lamenting the state of the startup fundraising environment or joking about hedge funds’ activity in venture, myself included!

The hedge fund most often in the crosshairs is Tiger Global — a tech-focused “crossover" that has dominated media headlines & VC gossip circles for the last 12 months due to its record-breaking deal pace & aggressive style. From an outsider’s perspective, Tiger’s investment strategy can be roughly summed up as:

Be (very) aggressive in pre-empting good tech businesses

Move (very) quickly through diligence & term sheet issuance

Pay (very) high prices relative to historical norms and/or competitors

Take a (very) lightweight approach to company involvement post-investment

Above all, deploy capital, deploy capital, deploy capital

And Tiger isn’t the only fund employing this type of strategy. Addition (led by ex-Tiger Global Partner Lee Fixel), Coatue (a “Tiger Cub”, just like Tiger Global), and several others exhibit these tactics to varying degrees2, and have elicited similar amounts of frustration from more “traditional” VCs.

Ask 10 VCs for their thoughts on Tiger et al and most of them will react with a mix of dismissiveness and disgust. They’ll say that crossovers are drastically overpricing rounds, not doing enough diligence on their investments, or are in some other way breaking the spoken & unspoken “rules” of venture. So what gives? Are Tiger & this new class of crossovers collectively dumb and/or drunk off of the spoils of a decade+ long tech bull market?

Not at all. On the contrary, we are seeing the emergence of a new velocity-focused strategy in the venture/growth3 asset class that will fundamentally change the way that venture capital is raised. By breaking many long-held but outdated rules & norms of venture/growth investing, Tiger has developed a flywheel that enables them to offer a better/faster/cheaper product to founders while generating more $ gains than their competitors. Tiger is eating VC, and with the right context, I think it’s clear why4.

Playing Different Games

There’s an amazing scene in Game of Thrones’ first season where a mercenary named Bronn fights a knight named Ser Vardis in a “trial by combat”. Bronn fights to save one of the show’s troubled protagonists Tyrion Lannister from a death sentence, and more importantly collect a nice payday from Tyrion if he succeeds in saving his life.

As you’ll see, the contrast between their fighting styles is stark5. Ser Vardis fights, well… very knightly and proper, while Bronn scraps-and-brawls his way to survival. In the end, Bronn skewers Ser Vardis and tosses him out of the conveniently located floating-castle-garbage-disposal.

The scene ends when Lysa Arryn - the person who sentenced Tyrion to die in the first place - scolds Bronn for his fighting style and sets him up for one of the series’ great one-liners:

Lysa Arryn: You don’t fight with honor!

Bronn: No, but he did.

Even with his own life on the line, Vardis constrained himself to fighting by the rules of knighthood & honor, while Bronn did whatever he needed to do to survive and get his payday. Vardis and Bronn were playing two entirely different games dictated by two different sets of rules. Vardis was playing “Be a Knight”, Bronn was playing “Survive”. The result? Bronn - 1, Ser Vardis - 0, and free falling 5,000ft from the Moon Door.

When I watch that scene, I see a nearly perfect analogy to what we’re witnessing in the venture/growth market right now. A lot of VC funds look awfully similar to Ser Vardis, and their Partners have sounded eerily6 like Lysa Arryn these past months. “Ugh, does Tiger even do work on their investments?” “They move so fast we can’t even get through our diligence process.” “We only lost to Tiger because they outbid us!” Meanwhile, Tiger continues on unbothered, recently closing on the 2nd largest VC fund ever and flexing a 26% Net IRR for its private funds in a recent investor letter. The unfortunate truth for the Ser Vardis funds of the world is that capital markets are brutally competitive, and if they play “Be a VC” instead of “Survive”, nothing is going to stop Tig-Bronn from throwing them out of the Moon Door.

This begs the question though - if we look at venture/growth as a game, what rules - if any - do the participants have to play by?

Venture Rules

Venture/growth funds have duties to three stakeholder groups - their LPs (who give them money to invest), Founders (who let them invest in their companies), and their own General Partners/Managers (who they want to make rich(er)).

A fund’s duty to LPs is to generate acceptable returns, i.e. investment returns that meet the LP’s target benchmarks / expectations and result in the LP happily investing in subsequent funds.

A fund’s duty to Founders is to offer them an attractive enough “product” such that Founders choose to exchange equity in their businesses for the Fund’s cash over another competing fund’s cash.

A fund’s duty to its own Partners/Managers is to maximize their profits via carry dollars.

If we look at venture/growth investing as a game, the duties to LPs and Founders above constitute the game’s two immutable rules - you must follow/succeed at both in order to play. If you fail, you lose and can no longer play, either because you can’t raise more money or you can’t deploy the money you’ve already raised effectively. Beyond that, you’re free to maximize carry $ by any strategy/means necessary (within legality). Any other rules that you or other players in the game choose to follow are imaginary, and don’t actually need to be followed.

When we accept this framework, it becomes obvious that there are countless ways the game can be played, and the best strategies/tactics for winning the game can change and evolve drastically over time. The biggest losers in this paradigm of countless play styles are those who believe:

That there are more rules to the game than the two immutable rules

That they play the game the “right way” and that competitors playing differently are playing the “wrong way”

That the game is static, and stays the same over time despite changes to the macro environment, behavior of other players, etc.

On the other hand, for the ambitious, adaptable, feline-affiliated player, opportunities abound in this game. Tiger has introduced a new play style centered around velocity to disrupt the market and exploit their competition’s tendency to cling onto stale rules/norms.

Tiger’s Game

In the past two years, Tiger has developed an entirely unique investment platform in venture/growth based on Maximum Deployment Velocity and Better/Faster/Cheaper Capital for Founders. These two pillars represent the most significant development in venture strategy since the advent of the growth fund7, and the best way to explain their significance is by comparing the approaches to the “normal” approaches taken by the funds they’re disrupting.

Maximum Deployment Velocity

Normal Fund: I’m going to deploy this fund I raised over the next ~3 years, because that’s what funds are supposed to do and that’s what I told my LPs we’re going to do. Over these 3 years, I’ll just try to do the very best deals I can and maximize MoM / IRR.

Tiger: I’m going to deploy as much capital as I physically can at an 18% IRR hurdle rate8.

Most funds think about investing pace in terms of deployment schedules, i.e. “how long should it take for me to fully invest this fund I just raised?” Usually, this deployment period is between 2-4 years, and fund managers do their best to invest along this timeline9. After determining a deployment schedule, the fund focuses on maximizing returns on each investment in that period.

These two levers - deployment pace and returns - make up a fund’s eventual profits generated from any given year of investing/capital deployment:

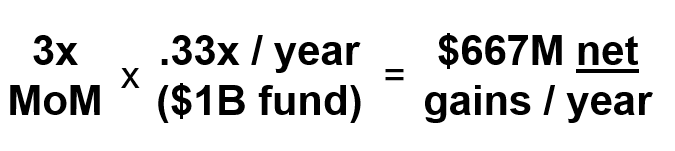

So if you raise a $1B fund, invest 1/3 of it every year (following a 3 year deployment schedule), and your investments are set to 3x as a blended basket at their exit, this is your cap gains equation for a single year of deployment10:

Looking good! Nearly $700M of total gains for a year of investing is nothing to sneeze at!

But what if, instead of investing on a 3-year deployment cycle, you instead deployed capital much faster, even if it meant that your returns were lower on average11? Your annual cap gains equation could look something like this:

Wow! Despite portfolio terminal MoM return declining an entire turn from 3x to 2x, you’re still making 1.5x the gains per year of deployment! That’s 1.5x more in profits in the accounts of your LPs, and 1.5x more carry dollars that your Partners take home to spend on Palm Beach real estate. As long as your LPs are OK with the returns you’re now generating on an IRR/MoM basis, you can make them more money with this higher velocity strategy, because they can invest more money with you instead of that municipal bond manager yielding them 2% a year12.

This is the first lever Tiger is using to disrupt VCs — while most funds still live in a world of deployment schedules, they threw the schedule out the window, and turned the velocity dial to 11.

This is important because it is extremely difficult for a fund to move to a maximum velocity strategy. To do so, you need:

LP buy-in — Investing faster means investing looser/with less discipline all-else-equal, and very rarely will LPs sign up for a strategy that will in all likelihood result in lower IRR & MoM. It takes an immense amount of trust with your LP base for them to give you the license/discretion to deploy capital this way. Tiger has two primary advantages here — the first is their strong 15+ year private fund track record, and the second is that collectively, Tiger’s own employees are its largest LP! This marries the interests of the Partners/Fund Managers and a big chunk of LP dollars, and is a far cry from typical venture funds, where Partners/Managers only make up 1-2% of invested capital in a fund13. So not only can Tiger’s GPs point to their 26% Net IRR since inception, they can also lead by example for external LPs and show that a large portion of their own money is at risk alongside theirs.

Fund ops that can scale to meet velocity — There is usually more to an investment beyond writing a check. A typical venture investment involves a pre-term sheet diligence process, ongoing board involvement from one or multiple Partners, and various other forms of portfolio company involvement. Intuitively, there are only so many boards a Partner can join and only so much work a team can handle. As the saying goes, “venture doesn’t scale”, and many firms simply aren’t built in a way that can handle a high velocity strategy. At first glance, Tiger also doesn’t look like the type of firm that could handle a high velocity strategy, as it’s not a large fund by headcount. Tiger has about ~20 investment professionals across its private and public funds (that's just over 1/3 of the investment team headcount of Andreessen Horowitz), and there are really only 3 Partners who call the shots / lead investments (Chase Coleman, Scott Shleifer, and John Curtius). So in order to handle their level of velocity, Tiger must develop an investment product that is drastically more scalable than the typical VC offering. This brings us to the second pillar of Tiger’s platform.

Better/Faster/Cheaper Capital for Founders

Normal Fund: When I invest in a business, I want to join the board so I can help guide the Founder and make sure we have a voice at the table - also doesn’t hurt to pad my LinkedIn ya know? ;-) We also only make a few large investments a year so I need to diligence the opportunity extensively — the founder shouldn’t mind, after all, this is a 5+ year relationship.

Tiger: VCs are rarely (if ever) helpful at the growth stage, so the best product I can offer founders is a high price (i.e. cheaper, less-dilutive capital), a quick & minimally distracting fundraise process, and to stay completely out of their way when we’re on the cap table. This approach also enables me to invest at high velocity despite having a lean team.

Just as startups build & sell products to their customers, venture/growth funds also develop products that they “sell” to startup Founders during a fundraise. Funds have to do this because fundamentally, what they offer is a commodity, money. They need other reasons for why a Founder would choose their cash over another fund’s. As the saying goes “we’re in the business of selling money.”

A fund’s product consists of everything that affects a Founder & business before, during, and after an investment process that stems from the fund. Today, a typical venture/growth fund’s product looks something like this:

2-4 week diligence process, including multiple calls with C-suite & function leaders, 3-5 facilitated customer introductions, an iterative list of data requests, etc.

A valuation that provides the fund with a strong base case return and a chance for a home-run outcome

The signaling / branding provided by the fund’s reputation

A board member (or multiple board members)

Other misc. investor “value-add” — access to the fund’s network, recruiting help, in-house operating/consulting teams, etc.

At first glance this doesn’t seem too bad! Unless of course the firm in question lacks strong market/brand signaling (as most do), their value-add is non-existent (it usually is), and the board member is neutral or even damaging to the board room / business (more common than it should be). Herein lies the second outdated (and false) norm/narrative that Tiger can exploit — the core pitch of most venture/growth products is built around the various areas of value-add that the fund will provide a startup, when in practice the funds provide little-to-no actual value. In fact, to many founders, I think the typical VC product can feel a little like this:

In contrast to this approach, Tiger offers founders a new product that takes the exact opposite stance on many of these features. I call Tiger’s product for Founders Better/Faster/Cheaper Capital (or B.F.C. Capital), and it looks something like this:

Extremely light diligence process, sometimes just one day with a single meeting and a P&L or any readily available financial data14

(Usually) the highest valuation offered by any large institutional fund — this means this is the “lowest cost of capital” option for Founders because the founder can raise more $ for the same amount of dilution or raise the same amount of $ for less dilution

No board involvement / very few touchpoints with the Tiger team

Access to Bain consultants if you want them for something

The faster and cheaper parts of B.F.C. are self-explanatory, but for many Founders, I also think the feature set above represents a “better” capital product relative to the norm15, because it lacks the potential downside that comes from a new highly-involved investor who ends up being more of a drag than a help, or even worse ends up being actively malignant to the board and business.

Is this product going to be the best fit for every single funding round or Founder? Of course not. But if you’re a Founder who already has the board members / investors that you want on your cap table, has little use for more “investor value add”, and is sensitive to dilution, wouldn’t B.F.C. be an attractive way to raise capital? I certainly think so.

And for Tiger, this approach is equally beneficial! We already established that Tiger needed to create a drastically more scalable venture product in order to scale its high velocity deployment strategy with their lean investment team. That’s exactly what the B.F.C. Capital product does — gone are time intensive diligence processes, ballooning board responsibilities, and in-house value-add efforts. B.F.C. Capital is an enabler for Maximum Velocity just as Maximum Velocity is an enabler for B.F.C., which gets us to the real special sauce of Tiger’s strategy — its emerging flywheel.

Summing Up - The Tiger Flywheel

Maximum Deployment Velocity and B.F.C. Capital are powerful because when used together they create a flywheel that enables a venture strategy that has never been used or seen at scale16.

In addition to their direct flywheel, both Velocity & B.F.C. Capital have their own flywheels in relation to the returns that the strategy generates. Here’s my best attempt at drawing out the what that looks like:

It’s no Amazon flywheel, but the significance here is that venture/growth is generally devoid of flywheels / sustainable competitive advantages / moats, excluding those driven by brand (which are rare).

With the Velocity<>B.F.C. flywheel intact, Tiger can offer Founders higher valuations than their competitors, and make substantially more investments than their competitors, driving superior $ investment gains. Tiger has developed the first structural, non-brand driven competitive advantage and flywheel at scale in venture. And they did it by throwing away a bunch of stale norms and made-up rules about how venture/growth should be practiced, and replacing them with a system that enables them to outcompete VCs on their own turf. That is why Tiger is going to eat VC.

Market Implications

While I’ve tried to hammer home the compelling aspects of Tiger’s strategy here to make my general point, they won’t be taking over the entire venture/growth asset class anytime soon. At the early stages of a business, a strong set of board members and core investment firms can be immensely helpful and improve a startup’s probability of outsized success a lot. I’d also argue that signaling/brand value is still the single greatest value add an investor can provide a startup, and that raising a round from FF/Sequoia/a16z/etc. is still more beneficial than a good price & fast process at nearly any round.

Ultimately & over time though, similar to what’s happened in retail over the last decade+, we’ll begin to see a middle squeeze in venture/growth. The most funds most insulated from the effects of this squeeze will be akin to

Luxury retailers (Apple, Sephora, Tiffany & Co.) — either via longstanding brand power (FF/Sequoia/a16z/etc.) or vertical focus/mindshare (Ribbit in Fintech), OR

Low-cost vendors (Walmart, Dollar General) — via high levels of scale and velocity driven by aggressive GPs, similar to Tiger (Addition, Coatue, etc.)

The most exposed and vulnerable will be funds stuck in the “middle”. When choosing between capital providers, sometimes Founders will want the $12 Amazon Prime 1-day-shipping Carhartt T-Shirt, sometimes they’ll want the $1,500 Gucci Cardigan, but very rarely will they want the $22 J.C. Penney Hoodie. You really, really don’t want to be the VC version of J.C. Penney.

And a lot more funds are J.C. Penney-esque than would like to admit. Expanding on what I mentioned briefly up in the “Venture Rules” section, the J.C. Penney funds of the world are those who:

Lack top-tier brand / signaling value to Founders, which forces them to compete on Tiger’s playing field

Don’t continuously evolve their strategies to meet the realities of the competitive landscape and the macro environment

Insist that their traditional venture process is required for investing in the category, and that any other approach is doomed for failure

Over time, these funds will find it harder and harder to compete, their returns will decline, and many will be forced to close up shop.

Conclusions

People in venture/growth like to deride Tiger, but as is the case with many things that are mocked, I think this attitude stems from misunderstanding more than anything else17. What investors should be doing instead is trying to better understand Tiger’s actions/motives and the downstream effects they will have on the market. To review this specific exploration of Tiger’s strategy:

Tiger is playing a different game — Tiger identified several rules / norms / commonly held ideas in venture/growth that are stale & outdated and built a strategy to exploit the contemporary realities around those ideas at scale.

Norm: Funds should deploy capital along a pre-defined schedule and then work to maximize MoM. Reality: When executed well, GPs and LPs can both make more money from a higher-velocity strategy that ignores traditional deployment schedules, even if it comes at the cost of maximum MoM returns.

Norm: VCs generally add value to companies post-investment and VC value-add is a core part of any fund’s pitch to a Founder. Reality: VCs can cause as much harm as they can help, and they very rarely move the needle for a business after the earliest stages. Therefore, a hands-off investor approach is often more compelling to a Founder than the typical VC offering, especially when paired with a high valuation / low cost of capital.

Norm: Without an in-depth diligence process, investing in startups even at the growth stage is too risky and will end poorly for those that try. Reality: Diligence in categories like SaaS has never been more commoditized, and with the right amount of investment velocity you can de-risk the negative impacts of individual frauds/blow-ups on your portfolio via diversification.

Tiger will continue scaling because this is a great strategy — The Velocity<>Better/Faster/Cheaper Capital flywheel that Tiger has created is real, and will continue to enable Tiger to offer a compelling, low-cost of capital product to Founders. Barring a dot-com bubble-like crash, Tiger will continue to generate strong cash returns and take share of the overall private venture/growth asset class over time, due to this flywheel.

The victims of Tiger’s continued ascent will be J.C. Penney-esque funds stuck in the “middle” during the impending venture/growth middle squeeze — Many firms offer neither the signaling/brand association of the world’s best venture funds, or the speed & low cost of capital of Tiger. Most of these firms have relied on a relatively less competitive venture/growth market over the past decade to generate compelling returns, and are not built in a way where they can adjust to these new competitive dynamics. Unless they make drastic changes to their strategy, internal processes, and org structure, they are destined to decline over time and eventually fail entirely.

Don’t worry too much about the Partners at the J.C. Penney funds though - this shift will happen gradually, and they’ll still make plenty of money-making investments before Tiger et al can eat their lunch entirely. They’ll still be able to afford a nice cabin in Tahoe to go with their Mill Valley home, though it may have to be in *gasp* Truckee instead of on the lakefront. But if you’re an associate at a fund that fits the “stuck in the middle” profile? Run away as fast as you can — because there’s a fight starting, and in the end the spoils of war are going to Bronn of the Blackwater.

Appendix I — Other Tiger Enablers

The surface area of strategy & tactics within capital markets is immense, and I’ve attempted to keep my focus as narrow as possible on what I think are the most disruptive & strategy-driven aspects that enable Tiger’s platform and competitive position. There are many more internal and external enablers, though, that are worth pointing out, including:

Increased business / returns predictability in the venture/growth category — Tech business models like SaaS have become much more well understood by the investing community in the last 5 years, as have the growth levers for these businesses and the methods for valuing them. With increased predictability comes less need for a large “margin of safety” from LPs. Instead of insisting on a 5x MoM from GPs due to the inherent volatility / unpredictable nature of venture/growth returns, LPs have increasing confidence in a lower band of outcomes and in some instances are moving toward a lower return, IRR-based hurdle rate when evaluating funds.

Tiger’s absolute scale — By last estimates Tiger Global has ~$65B of AUM, and as of their last 13F held about ~$5B of JD.com stock which alone is larger than most venture firms’ entire AUM. There are natural advantages and competitive distortions that come with this level of scale. For example: a $15-30M Series B check may be a massive deal to a $500M fund, but for Tiger it’s a rounding error. So Tiger can invest with less work and at a higher price vs. the $500M fund, because those $ matter less to them. It’s still worthwhile for Tiger to do this, though, because the option value of investing much larger dollar amounts in a subsequent round is massive.

The Grind — Most investors at hedge funds work at a sociopathic pace, especially relative to the west-coast cultures of most VC firms. It is very hard to regularly compete against a team of people who work ~16 hours a day 6-7 days per week.

Appendix II — On Market Returns

In this piece I’ve shied away from commenting on the state of venture/growth returns as a whole and where I think they’re going. An easy counter-argument to make against what I’ve laid out above is “Valuations are way overheated, because Tiger pays the highest prices they will be hit the hardest when the crash comes, therefore this is all irrelevant.” Sure! There is definitely a possibility that a big enough crash happens in private/public tech equities such that Tiger is severely impacted. But how many of you thought that day had arrived on March 20, 2020, right before the NASDAQ nearly doubled in a year? I believe making broad stroke predictions about forward market returns are a fool’s errand, and it’s more interesting to focus on the competitive dynamics that exist within the market regardless of the valuation environment.

My argument is that on a relative basis, Tiger is still at an advantage vs. the vast majority of funds in any market environment. If a big crash happens, every market participant will be impacted, and LPs will likely not like the way the vintage pans out whether you are Tiger or not.

Big thank you to John Luttig, Rick Brubaker, Josh Coyne, and Delian Asparouhov who provided me feedback and ideas during the drafting process.

Overheard conversation between two VCs who underperformed the Bessemer Cloud Index with their last 3 funds

I’m purposefully leaving Softbank out of this. It’s a very different strategy as will hopefully become clear

“Venture/growth” in this piece refers roughly to Series B and beyond, and I’m really referring to that section of the market in this piece. I know some hedge funds have started to creep earlier but I think the points of this piece mainly have to do with Series B to Pre-IPO

I’m going to focus singularly on Tiger in this piece for simplicity/flow, but the general points extend to these other firms to varying degrees

Meaning the “Venture-Growth” fund, such as Mary Meeker’s Digital Growth Fund at Kleiner Perkins which she started in 2011

This 18% IRR figure is totally made up & arbitrary - I have no idea if this is the hurdle rate that Tiger uses, but it would certainly be a good enough rate for most LPs to be happy

I have personally witnessed as well as heard several accounts of investors who liked an investment opportunity, but didn’t end up doing the deal because they were “well ahead of their deployment schedule”

To make the math / calc easy to understand, I’m using MoM instead of IRR, and I’m not specifying how long it takes to get to the terminal 3x MoM. Timing & subsequent IRR obviously matter a lot but including that would probably be more confusing than helpful for the point I’m trying to make

Another way to accomplish this would be to raise a bigger fund and deploy that bigger fund in the same timeframe as the smaller fund. This has definitely been happening over time in venture, but not anywhere close to what we’re seeing with Tiger

This isn’t necessarily true given that many institutional LPs have % allocation targets for different asset classes (e.g. 15% of funds go to VC, 20% to real estate, etc.), so you’d actually be competing with allocation to other venture/growth funds, but I think it’s safe to say that there is WAY more demand from LPs for quality venture/growth than there is supply, so most LPs are likely happy to get to increase their exposure to the asset class. This is also another reason why Tiger’s own employees being its largest LP is a big advantage

Notable exceptions include Founders Fund, Social Capital, Khosla Ventures

I’ve even heard of instances where they’ve offered a term sheet on the spot during a first call

Altos Ventures Co-Founder Ho Nam has a good counterargument against this type of product for Founders which you can find here - I disagree with him generally but think he’s absolutely right that this can also happen in individual circumstances

For those of you saying “What about Softbank!” you haven’t been paying attention

Jude 1:10

Brad G at the All-in summit just said... the thing about Tiger is you have to understand they were playing a different game... you have to know the game you are playing

Lee led Series A of one of our portfolio companies and Addition just invested in another of ours. I definitely think your article nailed it. The cubs are in a different game, especially when it comes to late-stage rounds. On the other hand, Lee is also very good at early stage. Maybe it's just the animal instinct of these hedge fund guys that happen to work perfectly in this massive capital supply era created by the Fed. In any case people with a skin in the game cannot rest.