Wave - Building a Cashless Africa

A new global fintech platform emerges

Today, Wave announced their $200M Series A, led by Founders Fund, Stripe, Ribbit, and Sequoia Heritage, and I am freaking stoked. Not just because we’re investing (though I am very happy about that), but because that $200M is going toward building financial infrastructure that could one day improve the lives of 1 billion+ Africans.

Since its introduction over a decade ago, mobile money has transformed how money is moved in Sub-Saharan Africa and has provided millions of Africans access to essential financial services. Historically, though, the market has been served by telecom companies offering products that are prohibitively expensive and deliver terrible end-user experiences. Wave is fixing this problem by building a full-stack mobile money platform that is better, faster, and radically cheaper than incumbent offerings. If Stripe's mission is to increase the GDP of the Internet, you could say Wave’s is to increase the GDP of Sub-Saharan Africa via affordable, high quality, widely accessible financial infrastructure.1

Millions of users in Senegal, Côte d'Ivoire, and Uganda already use Wave to deposit, withdraw, send/receive money, and pay their bills; saving ~70% compared to using telco-owned products. In Senegal, Wave has already surpassed the telcos as the country’s largest mobile money player and most of the country’s adult population use Wave every month. In coming years, Wave will continue to expand to new countries and offer more financial products, bringing Africa’s best and most affordable consumer fintech platform to users across the continent.

We rarely write long-form about the businesses we invest in, but Wave has stayed relatively under the radar to-date, and it’d be a shame for people to remain ignorant of one of the most fascinating emerging stories in fintech. A novel financial system, taking on big sleepy incumbents, democratizing access to financial services, insane growth — Wave has something for every fintech/startup/business nerd out there, and it’s still in the earliest days of its journey.

So read on if you’re curious about mobile money & Wave’s emergence as the leading challenger in the market, or even better consider joining Wave on their mission and witness it firsthand!

Wave — Building a Cashless Africa

Understanding the Wave opportunity involves understanding why the mobile money market in Sub-Saharan Africa (SSA) is so exciting, as well as why Wave is positioned to become a market leader across the continent. We’ll break out the answers to those questions in a sort-of-memo, sort-of-primer, sort-of-story format as follows:

Why this Market?

Mobile money is and will continue to be the dominant financial services modality used across Sub-Saharan Africa

African mobile money (while already a large market) is in the early innings of a multi-decade growth story, and the market is currently served by archaic & expensive incumbents

Why Wave?

Wave is run by an exceptional team who 1) is obsessed with building the best mobile money experience ever created, and 2) has already built a large consumer-facing fintech business in Africa

In a short period of time Wave has brought an offering to market that rivals the best consumer fintech products across the globe

Mobile money is a network-building wedge that enables Wave to create a platform for financial services spanning consumers & businesses across Sub-Saharan Africa

Why this Market?

Africa — The “Enduring Epicenter of Mobile Money”

Since the advent of Uber, Apple Pay, and most of all our beloved Starbucks App, Americans have become accustomed to paying for things with our phones. But did you know that you could pay for a cab ride with your phone in Nairobi, Kenya, years before you could in New York City? How, you ask? With mobile money.

“Mobile money” refers to a digital payments system that enables the transfer of money between mobile phones. Mobile money users can deposit, withdraw, send & receive money from their phones without being connected to the formal banking system.

M-PESA - the first major mobile money service in Africa - was launched by Safaricom & Vodafone in 2007, a full two years prior to the founding of Uber and in the same year that the the first iPhone was released.2 Since then, mobile money has rapidly grown to become the primary model for consumer money movement across Sub-Saharan Africa, and over 550 million mobile money accounts have been registered in the region.

Mobile money offerings have a few defining attributes:

Mobile-based accounts: Accounts are linked to a mobile device rather than an account at a bank. Devices can be basic SIM-based phones or smartphones.

E-money separate from the formal banking system: Mobile money providers issue customers mobile money credits in exchange for cash, with a guarantee that the customer can always withdraw their funds / redeem credits back to cash. (The actual cash deposits are held by partner bank(s).)

Agent networks: The backbone of mobile money platforms are networks of “agents” – individuals that run small kiosks/booths who are recruited and trained by the mobile money provider and paid via commission. These agents act as “live ATMs” from which users can deposit into or withdraw from their accounts or facilitate a money transfer/transaction. As of 2018 M-PESA had had 110K+ agents across Kenya, over 40x the number of bank ATMs in the country!

Direct access to popular payment types: Beyond P2P money transfers, users can often use their e-money credits directly to purchase mobile data, pay utility bills, take out or pay back a loan, etc.

Mobile money products come in various forms, determined by the mix of vendors performing essential mobile money functions. Vendor types include telecom companies, banks, and independent fintech companies.

All of the largest mobile money operators today are telecom-dominant models, and operate as subsidiaries of mobile network operators (MNOs) such as Safaricom, MTN, Orange, and Airtel (which make up the “Big 4” of SSA mobile money).

“Mobile money .. is not just a cool app. It’s a killer app, the first for mobile phones in the developing world. In five years, 19 million Kenyans, more than 70% of the adult population, have signed up for mobile money services [quote from 2012]… It took 115 years for banks to provide their customers with 43 licensed commercial banks, 1,045 bank branches and 1,500 ATMS; in roughly 5 years, Safaricom has provided its customers with more than 30,000 M-PESA agents, where people can transform cash into e-money or e-money into cash.”

- Money, Real Quick: The Story of M-PESA (2012)

What makes mobile money special — far beyond a fun anecdote about paying for cabs in Nairobi vs. NYC — is that it has completely transformed how people in Sub-Saharan Africa access financial services. Across the continent it has replaced a formal banking model notorious for its sparse and inefficient branch/ATM infrastructure that left basic financial services out of reach for most citizens, to become the default way to move & interact with money digitally.

Take Kenya, for instance. In 2006 (the year before M-PESA launched), less than 20% of Kenyans were formally “banked”,3 despite banks existing in the country for well over 100 years. The problem was that the traditional banking business model didn’t align with the needs of the Kenyan people. Retail banks make their money by accumulating deposits and making lots of loans, and the average Kenyan’s relatively modest transaction/deposit volumes meant that banks couldn’t profitably build and maintain branches outside of the country’s most dense urban centers.

That might have been fine if Kenya was like Singapore, whose entire population lives in an urban area. But Kenya is not like Singapore — in 2006 more than 75%+ of Kenyans lived in rural areas! To access a bank, many Kenyans would have to travel for hours (with their cash on hand) to the nearest branch, an arduous and dangerous journey that could very well end in the branch being closed or non-operational. It’s kind of hard to imagine more friction in accessing basic financial utilities than what Kenyans (and the people of many countries in Sub-Saharan Africa) dealt with prior to mobile money.

Thankfully, this all changed with the introduction of M-PESA4 in 2007. While bank branches were sparse and hard to reach, most Kenyans owned a phone & regularly bought airtime from Safaricom (the creator of M-PESA). Safaricom also already had an established network of ~100K existing airtime/mobile data dealers across the country who they could enlist to build a mobile money agent network with great coverage, and without the costs associated with building out new bank branches.5

If banks couldn’t bring financial services to Kenyans, Safaricom would by putting access, quite literally, in users’ hands! After running an extensive pilot program, Safaricom launched M-PESA across Kenya with the crystal clear tagline “Send Money by Phone”.

It only took 5 years from launch for 70% of the adult population of Kenya to sign up for an M-PESA account (2007-2012). The product was simple to understand, transactions were fast and safe, and the agent network made access extremely convenient. In 5 short years, a majority of Kenyans had near-instant access to essential financial services such as deposits/savings and P2P money transfers that were previously available to only a small sliver of the population. The economic impact of this paradigm shift was dramatic — one often-cited paper estimates that the introduction of M-PESA lifted 2% of Kenyan households out of poverty.6

Today, mobile money is by far the most popular way for people to move money and access basic financial services, not just in its birthplace of Kenya, but across Sub-Saharan Africa. It’s structurally more accessible, more convenient, and less costly than traditional banking, and now benefits from networks effects driven by being the most popular way for people to send money to each other.7

Of the ~300 million global mobile money monthly active users (MAUs) in 2020, more than half live in Sub-Saharan Africa. In Kenya, the use of mobile money has become so prevalent that annualized mobile money transfer volume (almost entirely through M-PESA) has eclipsed >60% of GDP!

An example to contextualize this level of scale: PayPal’s US Total Payment Volume (TPV) over the last year was $672 Billion, 3% of the USA’s ~$21.5 Trillion GDP. That means on a % of GDP basis, M-PESA is roughly 20x the size in Kenya that PayPal is in the US!8

Given this absolutely bonkers level of popularity / penetration in Kenya, you may be wondering if most of the growth for African mobile money is in the rearview mirror. Thankfully, not even close. In fact, the mobile money growth story is just beginning.

African Mobile Money — A Multi-Decade Growth Story in its Early Innings

If you’re trying to build a massive, impactful business from scratch, it helps to build in a fast growing market. It also helps if the market you’re building in is large, but growth is much more important, since small markets that are rapidly growing can quickly become large markets (as Jeff Bezos hypothesized about the internet when he found out it was growing at +2,300% per year in the late 90s).

Generally, the faster and more durable its growth, the better the market. US E-commerce, for example, has been growing well over 10% a year for over two decades! As far as markets go, Bezos and Lutke picked a pretty great horse. But what drives strong, long-term market growth? Usually, it’s a secular shift or step function change in technology, consumer behavior, or macroeconomic conditions which increases a market’s addressable landscape of customers/revenue/profits over time.

In some exceptional cases, a market can benefit from multiple simultaneous step functions / secular trends that compound to produce even faster and more durable market growth. The “US social media” market, for example, benefits not only from the increasing number of people that own a smartphone, but also the fact that each smartphone owner is looking at their device for longer each day.

Mobile money in Sub-Saharan Africa is one such exceptional case that pushes the idea of simultaneous market growth drivers to its limit. Across the continent, the category is benefitting from various technological, behavioral, and macroeconomic tailwinds driving user and transaction volume growth that are likely to persist for decades. These include

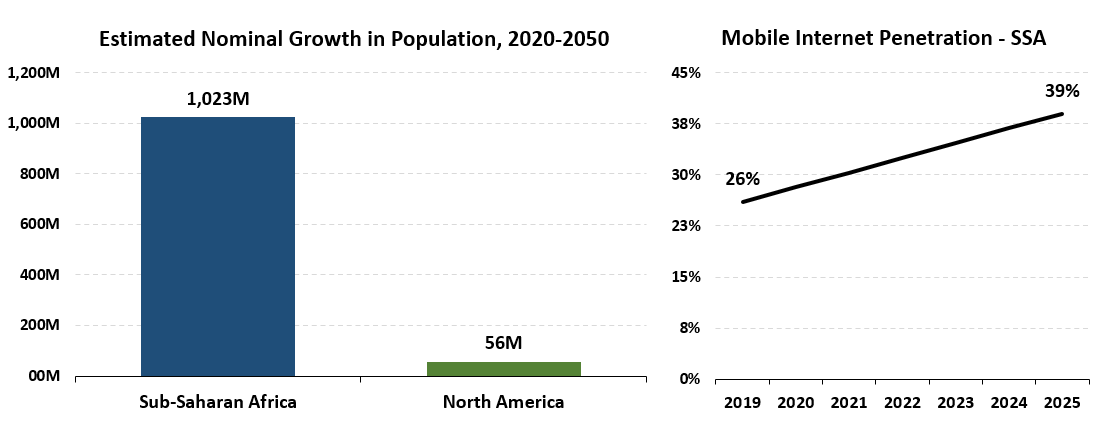

Rapid population growth across SSA, which has by far the largest projected increase in population between now and 2100 of any region globally

Steady increases in internet and mobile phone penetration rates across SSA

A growing share of Africa’s population rising into the middle class (i.e. increasing discretionary income per person)

Increasing preference for digital transactions over cash (which still dominates)

Expansion of mobile money product offerings to expand user access to more financial services

If one durable growth-driving trend is solid, and a couple is great, how do you even describe a market that has 5+ secular, compounding drivers of growth?

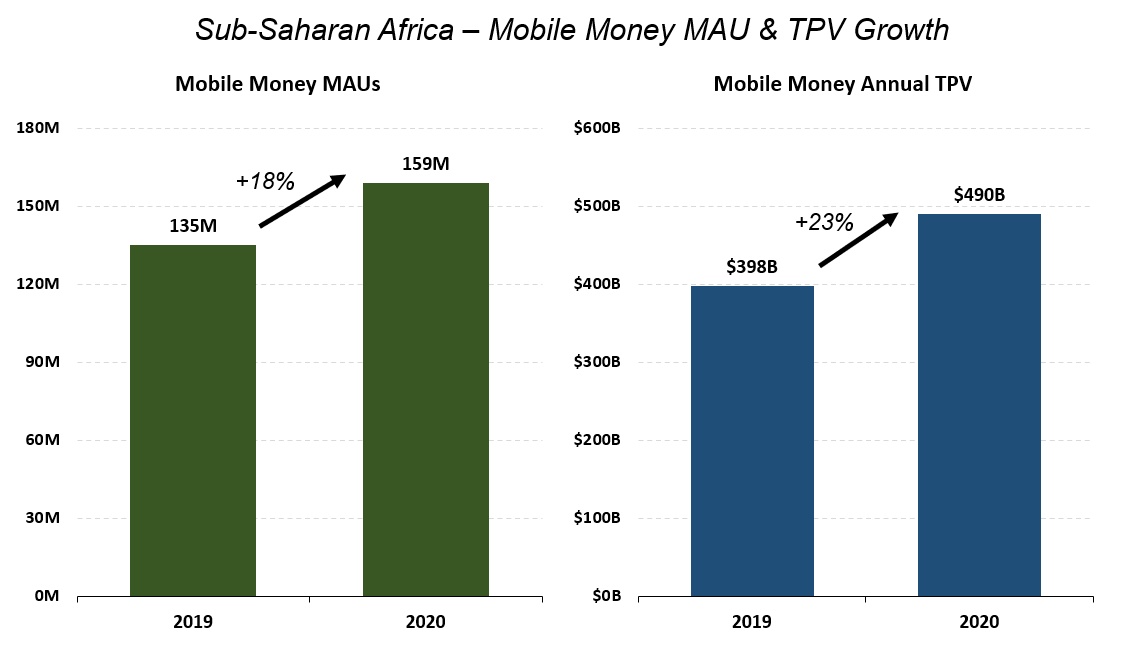

These drivers, along with increased adoption of digital payments during the Covid pandemic, propelled mobile money in SSA to grow +23% Y/Y on a total processed value (TPV) basis to nearly $500B in 2020, with ~160M MAUs (53% of all global MAUs).

And while some countries - such as Kenya & Tanzania - are already saturated from a mobile money user/account penetration perspective, many SSA countries remain early in their adoption of mobile money. As more people in these countries own phones, come online, begin commanding more discretionary income, and gain access to more financial services from mobile money vendors, user penetration will continue to rise rapidly. With a few exceptions, the other countries in the below chart should trend toward Kenya & Tanzania’s position in coming years.

There are dozens of mobile money operators of varying sizes serving this rapidly growing pie of users, but a few in particular have scaled especially well — the “Big 4” of Safaricom, MTN, Orange, and Airtel.

After Safaricom / Vodafone launched M-PESA and its success was evident, other mobile network operators quickly followed suit. MTN, Orange, and Airtel - all among the largest MNOs on the continent alongside Safaricom - created their own mobile money products and raced to replicate M-PESA’s success in Kenya across the continent.9 Today most of the Big 4 players offer mobile money products in 10+ countries, and to put it simply, business is a-boomin. In 2020, M-PESA, MTN’s Fintech arm, and Orange Money combined to generate $2.3B of revenue,10 growing +22% combined Y/Y. MTN’s fintech arm alone generated more revenue in 2020 than Silicon Valley software darling Snowflake, and generated more than 4x the revenue of Bill.com!

The incumbents’ stellar financial profiles illustrate both the strength of the market’s underlying growth drivers as well as their success in continuously expanding their mobile money products to new countries. But while these players have done a great job spreading mobile money throughout the continent, their products still leave much to be desired from a user’s perspective. Telco-operated mobile money is expensive, with high fees levied on users for withdrawals, money transfers, bill/utility payments, sometimes even just to check their account balance.11 And beyond pricing, the products themselves often still run on the same legacy technology they did more than a decade ago, which leads to reliability issues and confusing/difficult user interfaces. These shortcomings add friction to the mobile money customer experience, and often leave customers dissatisfied.

But what could the market look like if there was a service that delivered an excellent customer experience and low, transparent pricing? What increases could we see in the velocity of money movement and use of financial services in Africa if all the frictions associated with accessing them were removed? SSA markets are ripe for a contemporary market leader that brings innovation and customer obsession to the market and marries it with extreme affordability. Wave is emerging as that leader.

Why Wave?

Wave — When an A+ Team Meets an A+ Opportunity

“When mobile money succeeded in Kenya, it lifted about a million people out of poverty. And yet, over 10 years later, most Africans still lack access to affordable ways to save, transfer or borrow the money they need to build businesses or provide for their families. Wave is solving this problem by using technology to build a radically inclusive and extremely affordable financial network.” – Wave’s website

At Founders Fund, we focus obsessively on founder/team quality when evaluating an investment.12 In our investing process, we often ask ourselves “Why this team specifically? Why does this group of people have an unfair advantage in building this business for this market vs. anyone else?”

This is a particularly relevant question for a business like Wave. While the market opportunity is massive, building a full-stack mobile money challenger in Africa involves not just building an app, but navigating regulatory frameworks & obtaining licenses, negotiating bank partnerships, building and maintaining networks of tens of thousands of agents, and more. Not only that, but you have to do all of these things from scratch every time you enter a new country, with little cross-market synergies.

Basically, building a business in this market ain’t for the faint of heart — there are no APIs you can call to build/maintain an agent network of thousands, and there are no playbooks for launching a mobile money business from scratch that isn’t already attached to a mobile network business. To succeed, a team would need to have extensive experience in Africa, be filled with exceptional operators, and have the courage to build a full-stack, real world business that goes far beyond building great software (which is already pretty hard!).

Thankfully, the Wave team nails that combination. In fact, they were pretty much destined to build this business.

Wave was founded by Drew Durbin and Lincoln Quirk, who met as hallmates their freshman year of college and became fast friends. Spend an hour with them and you’ll understand why they were meant to build Wave - they’re smart as whips, extremely passionate about creating products that generate social impact, and have already founded & scaled a large fintech business in Africa.

That’s right, Wave isn’t even the first fintech business Drew & Lincoln have built to serve users in Africa. The first was Sendwave, an international remittances business providing reliable and instant money transfers to Africa from the US and Europe, that they created in 2014 after Drew got fed up with the high fees and general friction he experienced when trying to send money to his NGO in Tanzania.

Sendwave quickly became one of the largest remittance players on the continent, and in the process of operating that business, Drew & Lincoln made a fortuitous discovery. They discovered that the domestic mobile money products that their customers were using were just as broken as the products they were trying to replace in the remittance market. And unlike an intl. remittance product, people were using these mobile money products every day for every aspect of their financial lives, despite their obvious shortcomings.

They realized that while it’d be a much harder business to build, creating a full-stack mobile money platform was how they could make a truly massive impact on the lives of their users. So they sold Sendwave to WorldRemit about a year ago, and shifted their focus entirely to the mobile money opportunity with Wave Mobile Money.

The Wave team is now 800+ strong across their offices in Senegal, Côte d'Ivoire, and Uganda, and consists of a mix of exceptional local and international talent hell-bent on building the best fintech product ever created on the continent.

Wave — Africa’s Cash App

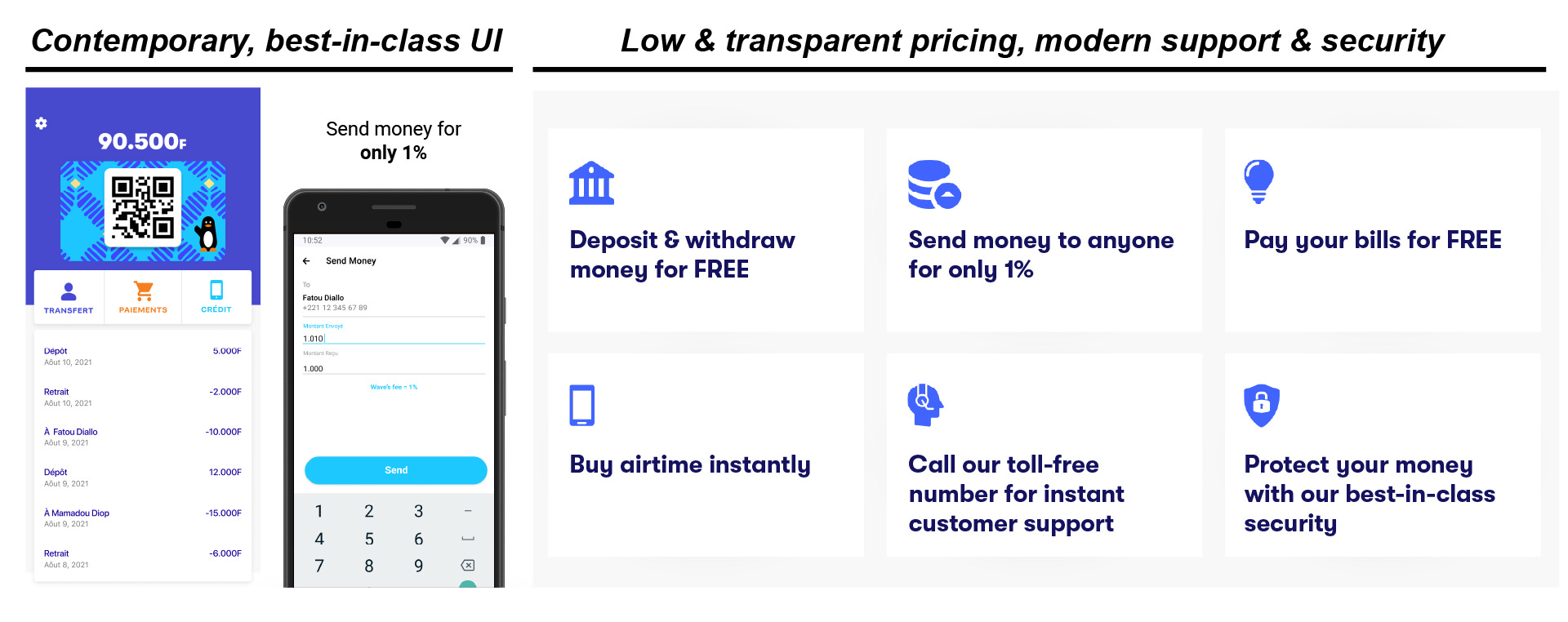

In a very short period of time, the Wave team has brought a product to market that rivals the best consumer fintech products in the US and around the world:

the product has a clean, intuitive UI,

app uptime / reliability is high,

customer support is friendly & helpful,

agents are accessible and don’t run out of money, and

the service is priced in a transparent and extremely affordable way - users pay a 1% fee for P2P transfers, while withdrawals, deposits & bill payments are all free13

In its current form, it feels a lot like Cash App (except you don’t need a bank account).

Maybe most impressive of all is the fact that Wave has been able to build & maintain a robust, high quality agent network from scratch in Senegal and Côte d'Ivoire without any of the built-in distribution advantages of an MNO — a testament to the team’s speed & quality of execution.

The quality of Wave’s offering shows in the stellar reviews and ratings it receives from its users & the insane user growth & retention they’ve experienced since launch. Online ratings and reviews for Wave are resoundingly positive, with users & prospective users urging the team to expand to their home countries and add more features to the product. And in the ~year since selling Sendwave, Wave has scaled as fast as any consumer fintech business I’ve ever seen,14 growing to millions of MAUs and quickly becoming the leading mobile money vendor in Senegal.

In coming years, the Wave team will expand its offering to many more countries in SSA, leveraging their learnings from building & scaling in Senegal, Côte d'Ivoire, and Uganda to better serve the rest of the continent.

New markets aren’t the only exciting way that Wave can expand, though. For markets like Senegal where Wave has established strong network effects & clear market leadership, the team can already start to think about what other financial products they - and others - can build for users on top of Wave’s core platform.

The Future of Financial Services in Africa

Today, Wave is focused on maintaining high quality infrastructure to support critical economic transactions, like deposits, withdrawals, bill payments, and P2P money transfers. But as its user network reaches critical mass in each country, Wave is in an incredibly strategic position to build more products on top of its core platform. If people are using your product every day to manage and move their money, why not provide them better ways to save and invest that money? Or buy things online straight from their mobile wallet? Or take out a loan to start a business?

And beyond offering their own incremental products, by creating and maintaining the building blocks for financial transactions as well as the network of users conducting those transactions, Wave is creating the foundations for Africa’s first fintech platform of scale, which represents a far larger opportunity than Wave exclusively offering products on its own.

Think about software in the US — the biggest step function change for that market in the last two decades wasn’t the emergence of SaaS applications but the emergence of AWS & the public cloud. By providing convenient, affordable, high quality infrastructure that removed many of the frictions associated with maintaining an application, AWS led to a proliferation of software businesses which have created Trillions of dollars of value in aggregate. AWS’ reward as the primary platform enabling this value creation? A cool $50B+ in annualized revenue.

What AWS did for software businesses, Wave has the opportunity to do for potential fintech & fintech-related businesses across Sub-Saharan Africa.

What new businesses can be created when you give entrepreneurial people cheap and convenient access to financial primitives that can instantly reach a majority of their country’s population? What specifically will be built on Wave’s infrastructure and by who? I have absolutely no idea. I am convinced, though, that like AWS, Wave could lead to a proliferation of fintech innovation and business creation in Africa that creates billions of dollars of value & improves millions of lives.

An Extremely Effective Way to Improve the World15

For all the reasons outlined above, Wave is emerging as the only viable challenger in a massive, underserved mobile money market with limitless upside & potential impact. If Wave succeeds, it will become one of the most important consumer fintech brands in the world, alongside the likes of Nubank, Cash App, Klarna, AliPay, Toss, etc. And more importantly, it will create immeasurable value for the people of Africa.

Every day, the Wave team is building & shipping products that make large, tangible improvements to the lives of millions of users. So if you’re looking for an extremely effective way to improve the world, or just want to join an absolute rocket ship startup with massive remaining upside, check out Wave’s career page and consider joining them in creating a Cashless Africa.

Additional Reading

This was already a lengthy piece, but we’ve only scratched the surface of all the interesting & exciting things happening in the African tech ecosystem. If you’re interested in learning more about mobile money, the African fintech market, etc. I suggest checking out the following links:

The “M” in M-PESA stands for m or mobile, and “Pesa” is Swahili for Money

This site from the World Bank gives some good introductory context on why financial inclusion (in the form of banking or otherwise) is so critical and the improvements it makes on the welfare of a population relative to exclusively cash-based communities

Fun anecdote: In 2002, researchers observed that across several countries, people were spontaneously using airtime credits as a proxy for e-money. Kenyans would transfer airtime to their relatives or friends who would then either use it or resell it to others, essentially creating their own mobile money system! This led to the pre-cursor of M-PESA

Mobile money agents were/are paid via a variable commission model, removing much (but not all) of the fixed costs associated with building/scaling a network

If you’re interested in a deeper dive into the story of M-PESA, I highly recommend reading “Money, Real Quick: The Story of M-PESA”

Long before “Can I Cash App you?” there was “Can I M-PESA you?”

A common refrain from VCs/investors is that “Sub-Saharan Africa’s GDP is too low to sustain large businesses, markets, etc.” (SSA’s GDP is ~$2T compared to the USA’s $21T). What this argument misses is how prevalent / dominant winning systems & products can become in Africa relative to a country like the US. M-PESA’s volume in Kenya is equivalent to 60% of Kenya’s GDP (and growing), whereas Visa’s total credit/debit US volume was equivalent to 22% of US GDP in 2020 (M-PESA’s revenue take rate on TPV is also much higher than Visa’s, so not even a fair apples-to-apples comparison for M-PESA).

Expansion for these businesses is a country-by-country undertaking. You can’t just “turn on” your mobile money product in a new country — you need to build out an agent network, secure relevant licenses, find a local partner bank to hold deposits, etc.

Mobile money operators generate revenue via fees levied on user actions like withdrawing money from agents, transfers, bill payments, etc. as well as by earning interest on the deposit balances they build for their bank partners

Check out MTN’s Uganda Mobile Money fee/pricing sheet for a full view of the types/amounts of fees users pay. Examples include:

A 5% fee for withdrawing $5 (~18K Ugandan shillings) from an agent

A 3% fee for sending $5/18K Shillings to another MTN user

A 13% fee for sending $5/18K Shillings to a non-MTN network

Fees for paying utility bills, school fees, TV payments, etc.

Hopefully this doesn’t come as a surprise given, you know, the name of the firm and all

Despite this radically affordable pricing model, Wave operates with strong/sustainable unit economics that continuously improve with scale

Seriously, out of all of the consumer fintech companies I have ever evaluated, Wave is the fastest growing at its scale

It always saddens me to see foreign-led companies raking millions on the continent. Africans need to wake up.

Hello